Mortage Calculator

Advanced Mortgage Calculator

Initial Payment Breakdown

| Category | Initial Monthly | Total Lifetime |

|---|

Amortization Schedule

| Date | Beginning Balance | Principal | Interest | Extra Payments | Ending Balance |

|---|

Latest Mortgage Rates

We update this data frequently but still you can do your search for latest rates.

The Ultimate Guide to Using a Mortgage Calculator for Home Buyers

Purchasing a home is arguably the single largest financial commitment you will make in your lifetime. Navigating interest rates, down payments, and loan structures can feel overwhelming. That is where a reliable mortgage calculator comes in. By converting complex financial math into clear, actionable data, an online home mortgage calculator allows you to strip away the guesswork and confidently explore what you can afford.

Whether you are looking to determine your maximum home budget or calculate the long-term cost variations between loan options, using a comprehensive, multi-purpose payment calculator is your essential first step. Below, you will find our interactive tool designed to give you instant clarity on your future housing costs.

The Mathematics Behind a Mortgage Loan Calculator

While an automated home loan calculator does the heavy lifting for you, understanding the mechanics under the hood gives you a distinct advantage when negotiating terms with financial institutions.

Every standard fixed-rate loan calculator mortgage uses a specific geometric series formula to distribute your principal paydown and interest evenly across your chosen term. The baseline monthly principal and interest payment is derived using the following mathematical formula:

$$M = P \frac{r(1+r)^n}{(1+r)^n – 1}$$

To see exactly how this works in practice, let’s break down the variables required by a monthly mortgage calculator:

- $M$: Your total monthly principal and interest payment.

- $P$: The principal loan amount (the purchase price of the home minus your initial down payment).

- $r$: The monthly interest rate. Because lenders quote interest as an annual percentage rate (APR), you must convert this figure to a monthly decimal by dividing by 12. For instance, an interest rate of 6% becomes $0.06 / 12 = 0.005$ per month.

- $n$: The total number of monthly payments over the lifespan of your loan. For a standard 30-year mortgage, this equals $30 \times 12 = 360$ payments. For a 15-year alternative, it translates to $15 \times 12 = 180$ payments.

Step-by-Step Amortization Example

Suppose you use a house payment calculator to evaluate a $300,000 loan balance ($P$) with an annual interest rate of 6% over a traditional 30-year timeline ($n = 360$).

- First, calculate the monthly decimal rate: $r = 0.06 / 12 = 0.005$.

- Next, evaluate the growth factor: $(1 + 0.005)^{360} \approx 6.022575$.

- Substitute these values directly back into your core equation:

$$M = 300,000 \times \frac{0.005 \times 6.022575}{6.022575 – 1}$$$$M = 300,000 \times \frac{0.030113}{5.022575} \approx 1,798.65$$

Through this mechanical calculation, your baseline monthly principal and interest obligation resolves to $1,798.65$. However, your actual out-of-pocket housing costs will vary because real-world monthly bills incorporate extra escrow elements.

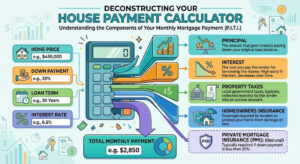

Deconstructing the Components of a House Payment Calculator

When home buyers use a home payment calculator, they frequently make the critical mistake of tracking only the base principal and interest amounts. Real estate professionals use the acronym PITI to outline the complete picture of your recurring mortgage footprint.

(Visual Representation: Mortgage Amortization Schedule Graph)

Understanding the internal structure of your payments transforms over time. In the early stages of a home loan, the vast majority of your monthly cash flow is directed toward satisfying the interest charges. As the remaining principal balance shrinks, the calculation shifts, allowing more capital to clear the principal and accelerate your equity growth. Since real estate acts as a primary wealth asset, modeling your home equity growth alongside other assets using a comprehensive investment calculator can help you coordinate your property purchase with your overall long-term financial strategy.

Let’s dissect the components that a robust monthly payment calculator mortgage tracks simultaneously:

1. Principal

This represents the direct reimbursement of the raw capital you borrowed from the bank. Every dollar assigned to the principal lowers your overall debt balance and increases your net home equity (the portion of the home you truly own).

2. Interest

This is the continuous premium you pay to the lender for utilizing their money. The interest amount is calculated dynamically each month based on your remaining unpaid principal balance.

3. Property Taxes

Local municipalities levy real estate taxes to finance community infrastructure, schools, and emergency public services. Lenders typically collect 1/12th of your annual property tax bill every month, parking it securely inside an escrow account to pay the municipality on your behalf when due.

4. Homeowners Insurance

Financial institutions require you to safeguard the property against hazards, structural fires, and natural disasters. Like property taxes, your annual insurance premium is divided by 12 and managed via your recurring escrow payments.

5. Private Mortgage Insurance (PMI)

If your initial down payment falls below 20% of the home’s total acquisition cost, lenders view the transaction as a higher-risk investment. To protect themselves from default, they will require you to pay Private Mortgage Insurance. PMI is typically added directly to your monthly statement until your outstanding loan balance drops below 80% of the property’s original appraisal value.

How to Budget Using a Mortgage Rate Calculator

Achieving long-term financial security requires analyzing how your new home payment blends into your broader household budget. When operating a mortgage rate calculator, underwriting institutions assess your financial profile using two primary debt-to-income benchmarks known as the 28/36 Rule.

- The Front-End Ratio (28%): This parameter states that your aggregate monthly PITI housing costs should not exceed 28% of your gross monthly household income (your pre-tax earnings).

- The Back-End Ratio (36%): This broader metric dictates that your total fixed monthly obligations—incorporating your new mortgage payment, credit card minimums, auto loans, student debts, and personal loans—should remain below 36% of your gross monthly income.

If you are carrying other outstanding monthly debts, calculating their structured impact with a dedicated personal loan calculator is a smart preliminary step to lowering your Debt-to-Income (DTI) ratio before applying for home financing.

Quantifying the Rules of Affordability

The following data table breaks down the maximum allowable monthly housing expenditures based on various annual household income brackets under the 28% front-end threshold.

| Gross Annual Income | Gross Monthly Income | Max Monthly PITI (28% Boundary) |

|---|---|---|

| $60,000 | $5,000 | $1,400 |

| $80,000 | $6,667 | $1,867 |

| $100,000 | $8,333 | $2,333 |

| $120,000 | $10,000 | $2,800 |

| $150,000 | $12,500 | $3,500 |

| $200,000 | $16,667 | $4,667 |

Pro Tip: While a lender might pre-approve you for a loan amount up to a 36% or even 43% back-end ratio, it’s wise to run your numbers through a mortgage payment calculator first. This helps ensure your new home payment fits comfortably alongside your long-term retirement planning strategies, personal savings goals, monthly utilities, and lifestyle choices.

15-Year vs. 30-Year Fixed Mortgages

One of the most important decisions you’ll make when using a home loan calculator is choosing your loan term. The vast majority of buyers choose between a 15-year fixed-rate framework or a traditional 30-year fixed-rate option. Both paths offer distinct long-term financial trade-offs.

Evaluating the Term Trade-offs

| Strategic Metric | 15-Year Fixed Mortgage | 30-Year Fixed Mortgage |

|---|---|---|

| Monthly Cost Footprint | Higher monthly payment requirements | Lower, highly manageable monthly payments |

| Assigned Interest Rates | Historically lower interest rates | Marginally higher base market rates |

| Equity Accumulation Rate | Rapid equity growth | Gradual, slow-moving equity build-up |

| Lifetime Borrowing Costs | Extremely low lifetime interest expenses | Substantially higher interest costs |

A 30-year term offers lower monthly payments, which maximizes your short-term cash flow and purchasing flexibility. However, because the debt stretches over a longer timeline, the total interest paid over the life of the loan is significantly higher.

Conversely, a 15-year term forces a much faster principal repayment schedule. While this requires a higher monthly payment, it saves you tens of thousands of dollars in lifetime interest and builds home equity much faster.

Strategic Tactics to Optimize Your Amortization Schedule

If you decide to take out a 30-year loan to keep your initial payments low, you don’t have to stay locked into a 30-year payoff timeline. You can use data from a mortgage loan calculator to implement smart payment strategies that shave years off your loan and save you thousands in interest.

1. The Power of Extra Principal Payments

By adding an extra payment directly to your principal balance each year, you can dramatically accelerate your payoff date. You can achieve this easily by taking your standard monthly payment, dividing it by 12, and adding that amount to your regular payment each month. This builds up to one extra full payment every year. For a standard $350,000 mortgage at 6.5%, this simple step can cut your loan timeline down from 30 years to roughly 25 years.

2. Shifting to an Accelerated Bi-Weekly Plan

Instead of making one standard payment a month, split your monthly requirement in half and pay it every two weeks. Because there are 52 weeks in a year, you will make 26 half-payments. This totals 13 full monthly payments over a 12-month calendar year. This seamless shift safely removes years of interest from your loan balance without requiring major changes to your budget.

3. Watching for Strategic Refinancing Opportunities

Keep a close eye on market trends using a mortgage rate calculator. If interest rates drop by 1% or more below your current rate, refinancing your loan could be a smart move. This strategy allows you to lock in lower rates, reduce your monthly obligations, or safely transition from a 30-year plan to a 15-year track without a drastic jump in your monthly costs.

Frequently Asked Questions (FAQ)

Why do some online searches spell it as a mortage calculator?

It is very common for people to accidentally type mortage calculator when searching for home finance tools online. Most modern search platforms and high-quality web calculators automatically recognize this minor typo and will still guide you to the correct tools without any issues.

Does an online mortgage calculator run a credit check?

No, online calculators do not connect to credit bureaus or run credit checks. They simply calculate the math based on the numbers you type in. This makes them a safe way to test different financial scenarios without impacting your credit score.

Should I trust a home payment calculator for all closing costs?

While a home payment calculator is excellent for estimating your regular monthly costs, it usually does not include upfront closing fees. When buying a home, expect to pay an extra 2% to 5% of the total loan amount for things like bank loan originations, property appraisals, title insurance, and legal fees.

How often do mortgage interest rates shift?

Mortgage rates fluctuate daily based on broader financial markets, inflation trends, and macro-economic policy shifts. Keeping track of live daily interest rate indexes on Mortgage News Daily regularly during your home search helps you see exactly how these market moves affect your future buying power.